DeFi Opportunities Fund Performance & Rebalance Note: January 2024

December Performance Estimates

100 Acre Ventures DeFi Opportunities Fund +4.8%

Ethereum: -10.1%

Top Contributors

Top Detractors

January Rebalance Overview & Ecosystem Observations

There was a lot of dispersion in the market in the month of December, both within DeFi as well as DeFi relative to the majors. The fund returned +4.8% with the median asset return being +1.4% vs. Ethereum -10.1%, BTC -3.1%, and SOL -20.4% in December. The top performing names in the fund were HYPE, MORPHO, and AAVE which increased 174.2%, 128.3%, and 45.7% respectively. The bottom 3 performing names were INJ, JUP, and SNX which fell -37.2%, -29.6%, and -27.2% respectively.

Another interesting observation is related to the portfolio vs. the eligible universe of assets. The fund held 23 names in December. There were 48 eligible names (universe names that met the volume and fully diluted network value criteria). The median return of those names in the portfolio was 1.4% vs. -18.17% for those names that were eligible but excluded from the portfolio as a result of the portfolio construction rules.

Portfolio Adds/Increases

Usual Money (USUAL) was added to the fund this month. It’s now the 7th largest stablecoin by circulating supply and the 3rd largest decentralized stablecoin. Current circulating supply stands at $1.77B and has grown at 132% month over month with ~$5.3M in trailing 90d fees. Ether-Fi (ETHFI) was another add. Ether-FI is a liquid staking protocol that provides yield from ETH staking and re-staking. The protocol also offers products like Liquid Vaults, which automate DeFi yield generation by allocating funds across integrated platforms such as AAVE, Pendle, and Uniswap V3, aiming to maximize returns for users. Ether.fi provides a secure and decentralized solution for Ethereum staking, enabling users to maintain control over their assets while earning enhanced rewards through restaking and DeFi integrations. It has generated $63M in fees over the last 90 days with month over month fee growth standing at 15%. DRIFT and DYDX also came back into the fund after seeing improvements in fee growth.

Portfolio Drops/Reductions

Hyperliquid (HYPE), which increased 174% in December, was reduced by about 2/3rds and started the month around a 2.5% weight. While the platform has shown solid statistics, with $283B in 90d aggregate volume, $85M in 90d trailing fees, and experiencing 38% in m/m fee growth, the price has appreciated much faster than the underlying statistics. It’s possible that we’ll see continued robust growth, as the narrative around hyperliquid has shifted from being the dominant perp trading platform to being a more generalized L1 that will compete with the likes of Solana. Currently, the fully diluted network value (FDNV) of HYPE is $25B vs. Solana at $129B. Within lending, AAVE (AAVE) and Morpho (MORPHO) were also strong performers MTD with price increases of 45.7% and 128.3%, but saw reductions in their weights for similar reasons as HYPE. Aerodrome (AERO) returned -13% on the month and was dropped from the portfolio. While it continues to dominate volumes within the BASE ecosystem, the volumes are highly subsidized. While trailing 90d fees are +$102M, net fees are -$75M highlighting the large token subsidy. It also saw negative growth in net fees over the last 30days.

Sector and Ecosystem Shifts

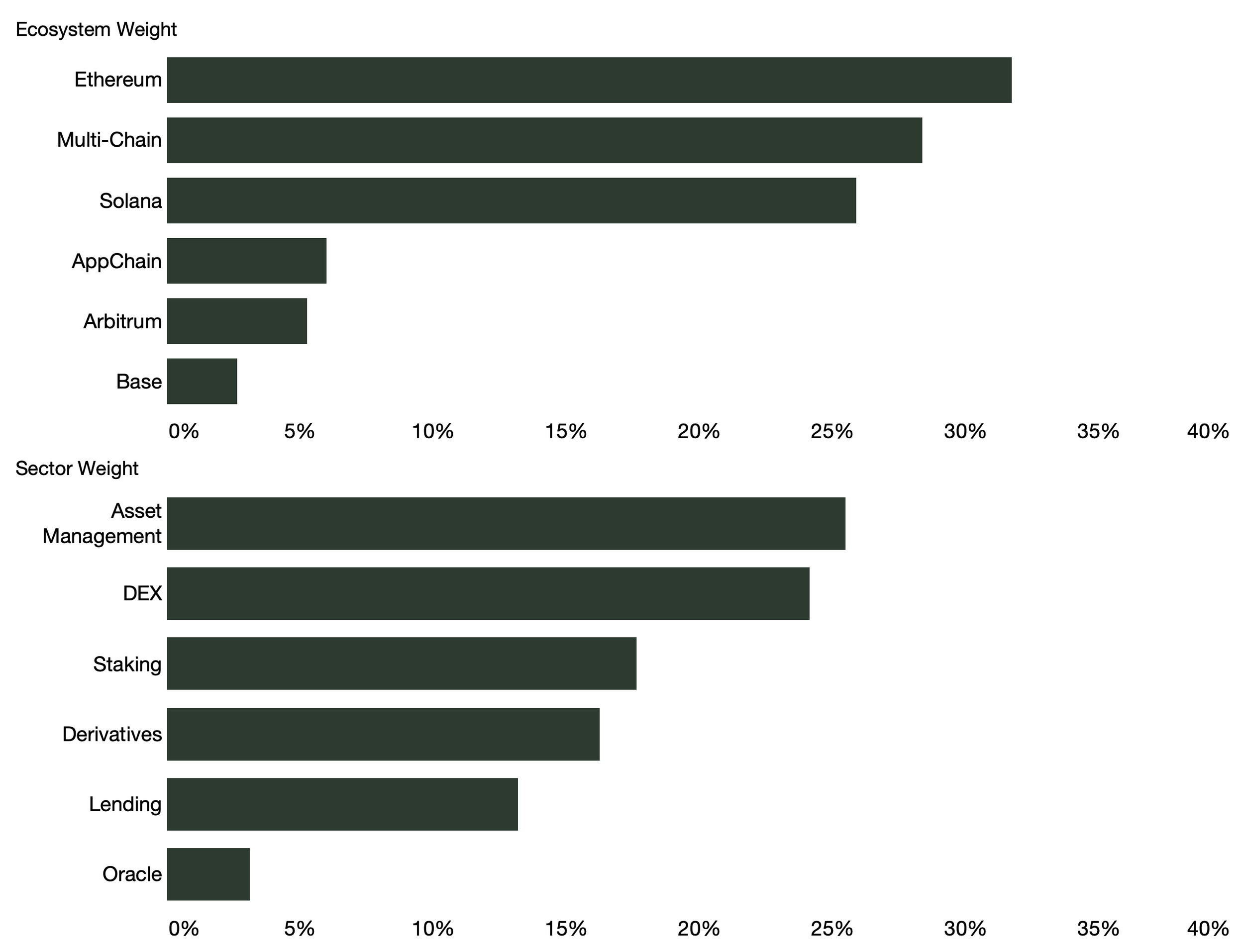

The largest sector weight increases are within Asset Management and Staking with the largest decrease in Lending and DEXs. The Ethereum ecosystem saw the largest increase in month over month exposure driven by the addition of USUAL. It’s worth noting that while we distinguish between Ethereum and Multi-Chain “ecosystems”, most all multi-chain dApps (UNI, AAVE, etc.) are multi-chain across EVM chains and generally accretive to Ethereum. From the launch of the fund in June, we’ve seen a steady increase in the relative weighting of Solana at the expense of EVM chains, but this has slowed in recent months with November representing “peak” Solana exposure since inception. An emerging trend that we’re actively monitoring is that of AppChains representing a larger share of overall DeFi economic activity.

One of the primary goals of the 100 Acre DeFi Opportunities Fund is to capture the holistic DeFi opportunity set. The constituents of the pro-forma portfolio capture 97% of the economic activity within DeFi (as measured by net fees), and through that lens the fund is achieving its goal.

When you break down economic activity by ecosystem, there are some interesting observations. About ⅓ of trading volume (spot + derivative) is now captured by AppChains, led by the growth in Hyperliquid and the migration of platforms like DYDX to the AppChain model. This trend is likely to continue with the launch of Unichain. Another observation is that the Solana-based dApps in the fund represent 11% of network value within DeFi but 53% of the total economic activity (as measured by net fees). Ethereum + Multi-Chain represents 53% of network value and 39% of economic activity as measured by net fees. The high net fees within Solana are driven largely by DEX trading, specifically speculative trading around meme coins and, more recently, agentic tokens. The Ethereum and the Multi-chain ecosystems are much more diversified, with Lending being a much larger driver of economic activity. The likely reason for this is the large concentration of stablecoins on Ethereum, which currently stands at $113B vs. $5.5B for Solana and remains a key factor in determining the ability of an ecosystem to support DeFi activity.

Following the January rebalance, here are the current ecosystem, sector, and position weights as of Jan 6th 2025.

Sector, Ecosystem, and Positions weights as of January 6th, 2025